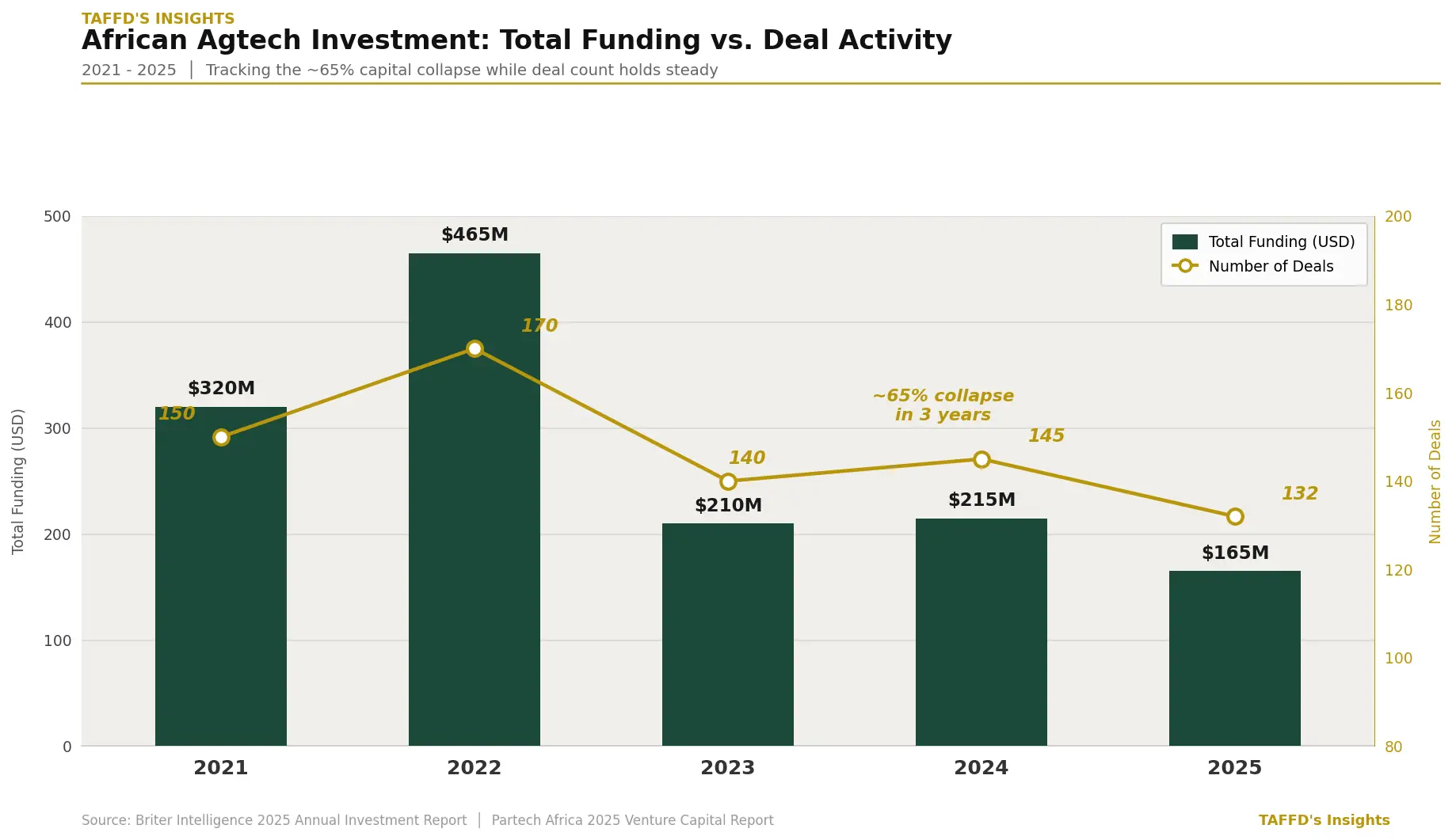

In 2022, investors deployed roughly $400 million into African agtech. By 2025, that number had fallen to approximately $165 million.

That is a 60% collapse in three years.

But look closer at the data and something unusual appears. The number of deals did not collapse at the same rate as the capital. Investors are still showing up. They are still signing agreements. They are still deploying money into the sector.

They are just writing much smaller cheques. And they are structuring those cheques very differently from before.

That gap between deal activity staying relatively stable while capital collapses is where this examination begins.

The money is changing shape

According to the Partech Africa 2025 Venture Capital Report, debt financing now accounts for 41% of all capital deployed in African tech. In 2019, that number was 17%. In 2025 alone, African tech startups raised $1.64 billion through debt financing. A 63% jump from 2024 and the highest level ever recorded on the continent.

Across fintech and cleantech, equity still dominates. Investors in those sectors are taking ownership stakes. They are sitting on boards. They are betting on upside. They believe in what those businesses are building and they are willing to wait for the return.

But in agtech and agriculture, the Briter 2025 Annual Investment Report shows a different picture. Asset-backed financing has become the preferred model. Investors are lending against specific assets (equipment, inventory, logistics infrastructure) and collecting predictable returns regardless of what happens to the business they funded.

When you take equity in a business, you are saying I believe in your future. When you structure asset-backed debt, you are saying I want my money back.

Could these two things be telling us the same story from different angles?

And what if they are? What if the shift from equity to debt is not a financing preference but a silent withdrawal ( investors staying visible in the sector while reducing their actual commitment to its future)?

What the data reveals when you connect the dots

Most analysts reading these numbers are calling it market maturity. The thinking is straightforward. Investors have moved beyond the hype cycle, they are being disciplined, this is what a maturing ecosystem looks like.

But maturity in investment does not produce this pattern.

When a market matures, equity deepens. Investors who understand a sector better take larger positions because their confidence has grown. They have seen the models work. They know what returns look like. They lean in.

That is not what the Briter and Partech data are showing together. What they are showing is investors leaning out while staying visible. Present but uncommitted. Doing deals but protecting downside at all costs.

Now connect that to a third data point.

The financing gap for agricultural SMEs and smallholder farmers across Africa currently stands at $117 billion. At the same time, ten companies captured roughly three quarters of all agtech funding in 2025. The capital that remains in the sector is concentrating at the top while the base (the smallholder farmer, the early-stage agtech founder, the on-farm innovation that feeds the continent) receives progressively less.

What if that $117 billion gap is not a market failure waiting to be corrected? What if it is the predictable output of a trust deficit that has been building slowly for years and the current data is simply the first time it has become large enough to measure clearly?

Three data sources. Three different pictures of the same sector. Could they be pointing at the same root problem?

Where the trust gap might be hiding

In African fintech, investors take equity because they can model the risk. Every digital transaction generates a data point. Investors can see inside the business in real time. They can build projections. They can price uncertainty into their valuation and still bet on the upside.

In African agtech (particularly on-farm) that data infrastructure does not exist at the same scale. Smallholder farmers operate largely informally. Yields depend on rainfall, government input supply, road conditions, and post-harvest infrastructure that breaks regularly. There are no standardised records. No digital credit histories. No consistent data trail that tells an investor what a farmer produced last season and what he is likely to produce next.

So investors do what rational actors do when they cannot price risk accurately. They stop betting on upside and start protecting downside.

Could the shift from equity to debt in African agtech be less about financing preference and more about a trust deficit that the data infrastructure of the sector has never resolved?

What if that trust deficit is not temporary? What if it has been structural all along and the post-2022 funding decline is simply the moment it became too large to paper over with optimism about Africa's growing middle class and rising food demand?

And if that is the root cause, what does it mean for everything built on top of it?

A pattern that could be heading somewhere dangerous

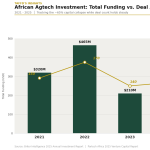

The Briter 2025 data shows something else beneath the funding decline. Investment is not just shrinking. It is restructuring. Capital is quietly moving away from on-farm processes (seed development, mechanisation, farm management, input supply) toward post-farm processes. Logistics. Warehousing. Food processing. Supply chain platforms.

Investors are following predictability downstream. The post-farm is easier to model. The returns are more visible. The assets are more tangible.

But the on-farm is where food is actually produced.

What if this restructuring continues for another three years at the same pace? What if on-farm investment keeps declining while post-farm infrastructure keeps growing, and Africa finds itself having built a more sophisticated supply chain for a harvest that is slowly shrinking? The pipeline grows more efficient. The water flowing through it reduces. At what point does the post-farm infrastructure have nothing left to process?

Could this pattern, if it continues through 2026 and beyond, begin to show up in food availability numbers?

According to the UN World Food Programme (WFP), over 55 million people in West and Central Africa are projected to face a hunger crisis during the June to August 2026 lean season. Nigeria alone accounts for 35 million of that projection.

What if that number is not just a food crisis statistic? What if it is also the early downstream consequence of years of capital withdrawal from the part of agriculture that actually produces food (a consequence that arrived before anyone finished debating whether the investment restructuring was a good thing or a bad thing)?

These are not separate conversations. They could be the same conversation at different stages of the same trajectory.

What this might mean for the people building in this sector

When investors hold equity, they are partners. They bring capital but also networks, market access, introductions, and follow-on funding signals that attract other investors. A founder with equity investors has people in the room with skin in the game.

When investors hold debt, they are creditors. They provide capital and wait for repayment. If the business struggles, they recover what they can from the assets backing the loan. The founder absorbs the rest.

In a sector already navigating broken infrastructure, currency volatility, climate exposure, and policy uncertainty. Could the additional weight of creditor pressure on top of operational pressure be enough to make rational, talented founders silently choose other sectors?

What if that is already happening? What if the founder pipeline into African agtech is not collapsing dramatically which would be visible and alarming. But, narrowing gradually, one rational decision at a time, in a way that only becomes measurable years after the damage is done?

What if the next generation of African agricultural innovators is already looking at the risk structure of this sector and choosing fintech or any other sector instead?

And if that is happening, then how would the continent know before it was too late to reverse it?

The questions this data is not yet answering

The numbers available today show a sector in structural transition. What they cannot yet confirm is whether this transition has a floor or whether the current trajectory continues until something breaks visibly.

2027 may be the year the data begins to answer that question. If on-farm capital continues its decline while post-farm infrastructure grows, and if food production numbers fail to keep pace with the supply chain being built to move that food. Then, the pattern will become impossible to read as maturity.

But by then, the window for early intervention may have already closed.

So the questions worth asking now are these.

What would it take to rebuild investor trust in African agtech at the on-farm level specifically. Not with rhetoric but with the kind of data infrastructure that makes equity investment rational again?

What if blended finance is the structural bridge? But if it only protects investors, not founders, does it merely shift the burden? Who will design a genuinely win-win structure (one that insulates founders, not just capital) before 2027 confirms what the data already signals today?

And what does Africa risk if this question is left to the market to answer alone?

This is the first in a four-part Prognosis Series examining the structural fault lines in African agtech investment. The second release examines the Pipeline Paradox (what happens when you build sophisticated downstream infrastructure for an upstream that is shrinking).