In our last examination, we identified a trust deficit hiding inside African agtech investment data. This examination follows that deficit downstream to where it is slowly building something nobody planned for.

In 2025, investors put more money into moving African food than growing it.

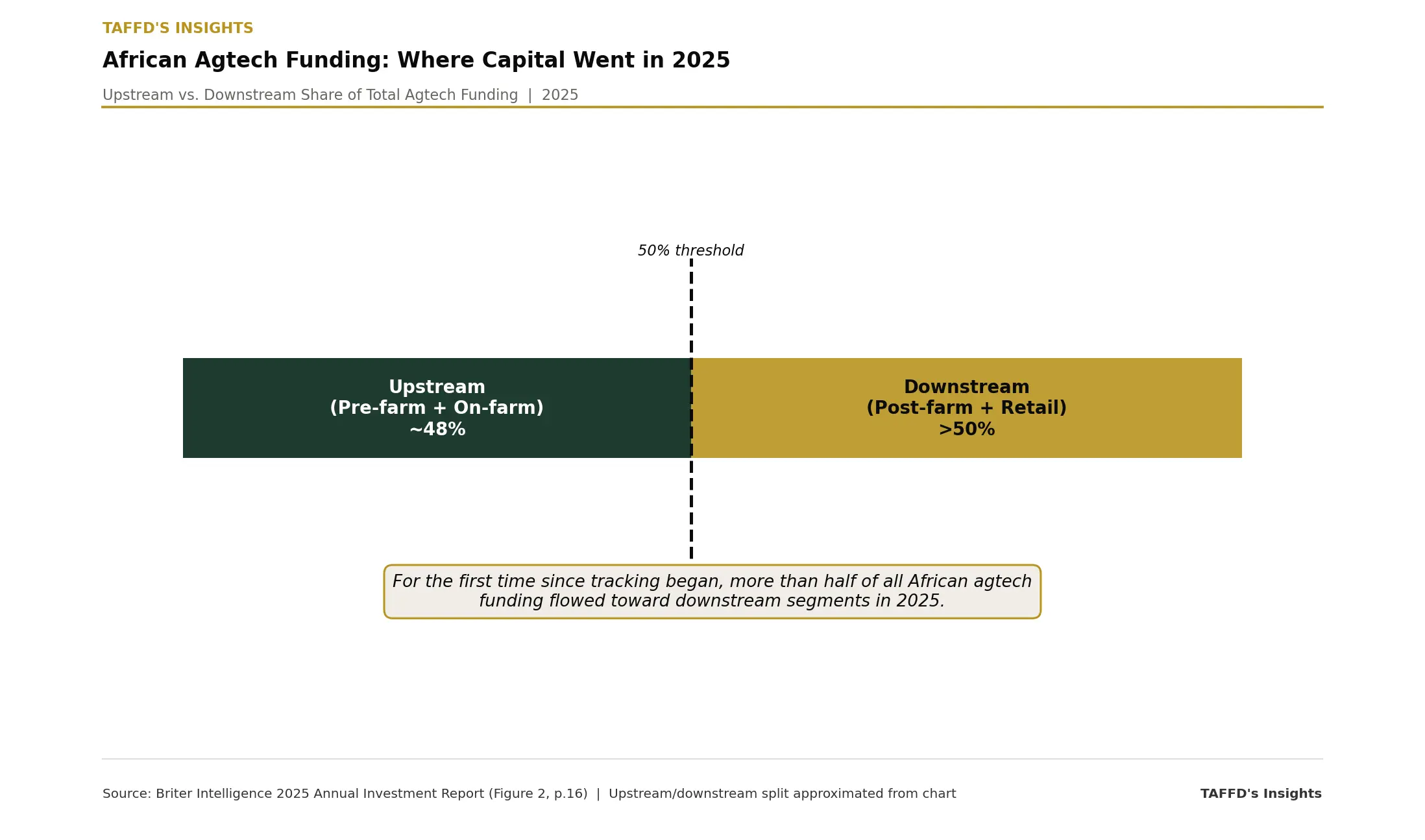

Post-farm processes (logistics, warehousing, food processing, supply chain platforms) accounted for approximately half of all agtech funding on the continent based on Briter's value chain charts. The year before, that share was closer to a quarter.

That shift happened in a single year.

At the same time, on-farm investment (the capital that determines how much food actually gets produced) continued its decline. 2025 was the first year since tracking began that both total funding and deal count in the sector declined simultaneously.

Africa is building a more sophisticated supply chain. The question nobody is asking is what exactly it is going to move.

The logic pulling capital downstream

The reasoning is not hard to follow. On-farm investment is difficult to model. Yields depend on rainfall, government input supply, road conditions, and smallholder farmer access to capital that rarely arrives predictably. Investors cannot price that kind of uncertainty with confidence.

Post-farm is different. The assets are tangible. The revenue streams are more stable. A logistics platform, a cold chain facility, a food processing plant. These are infrastructure plays with clearer return profiles.

So capital followed the predictability. Logistics networks connecting smallholder farmers to urban markets. Cold chain infrastructure reducing spoilage between farm and shelf. Food processing facilities converting raw agricultural produce into packaged goods. Supply chain management tools giving distributors real-time visibility across distribution nodes.

But the Briter 2025 Annual Investment Report shows something else happening at the same time. While post-farm investment surged, on-farm capital continued falling. Seed development. Mechanisation. Farm management tools. Input supply chains. The processes that determine how much food actually enters the system in the first place.

Could the capital be building the pipeline while slowly reducing the water flowing into it?

Two chambers. One system. One question.

Think of African agriculture as a system with two connected chambers. The first chamber is on-farm. It produces the raw output (the harvest). The second chamber is post-farm. It processes, moves, and distributes that output to where it needs to go.

For the system to function, both chambers need investment. A more efficient second chamber only delivers value if the first chamber is producing enough to fill it.

What the current data shows is capital concentrating in the second chamber while the first chamber receives progressively less. The infrastructure downstream is getting more sophisticated. The production capacity upstream is getting less support year after year.

At what point does the second chamber begin processing air?

According to the AgBase and Briter 2025 Annual Investment Report, around a dozen companies captured well over half of all agtech funding between 2016 and 2025. The capital flowing into post-farm infrastructure is not broadly distributed. It is concentrated in a small number of platforms with the existing asset base to attract debt financing. The thousands of smallholder farmers and early-stage on-farm innovators who determine how much food actually gets harvested are not among them.

What if the sophisticated supply chain being built today is calibrated for a harvest volume that peaked in 2022 (and the production capacity to sustain that volume is already slowly eroding)?

A gap that may be more than a financing problem

The financing gap for agricultural SMEs and smallholder farmers across Africa is estimated between $100 and $120 billion across IFAD, FAO, and IFC diagnostics. That number appears regularly in development finance discussions. It is almost always framed as an opportunity waiting to be filled.

But what if it is also a warning?

Could a gap that size, persisting long enough, begin to show up not in investment reports but in harvest numbers?

Every planting season that smallholder farmers enter without adequate capital access is a season of reduced mechanisation, lower input quality, and constrained yield potential. A more efficient supply chain gives farmers a better route to market. But if they cannot produce more (because the capital that would allow them to respond to better prices never arrived) a better route to market just moves the same constrained volume more efficiently.

The pipeline grows more sophisticated. The harvest stays the same. Or shrinks.

Could this be what the data is already signaling (not in a single dramatic event, but gradually, one underfunded planting season at a time)?

According to the UN World Food Programme, approximately 55 million people in West and Central Africa are projected to face a hunger crisis during the June to August 2026 lean season. Nigeria alone accounts for 35 million of that projection.

What if that number is not only a reflection of climate stress and macroeconomic pressure? What if it is also an early signal of a capital allocation pattern that has been slowly starving the upstream for three years while silently building the downstream?

And if both things are happening simultaneously (a hunger crisis arriving while post-farm infrastructure investment surges) what does that tell us about the relationship between where capital is going and where food security is heading?

An assumption that has never been tested at this scale

Post-farm investment rests on a specific assumption. That there will always be enough upstream production to justify the downstream infrastructure.

A logistics platform assumes there will be produce to move. A food processing facility assumes there will be harvests to convert. A cold chain assumes the volume flowing through it will justify the operating costs.

That assumption has never been tested at the scale currently being built.

What if it breaks?

What if on-farm capital continues declining through 2026 and 2027 while post-farm infrastructure keeps expanding (and African agricultural output fails to grow proportionally with the infrastructure being built to distribute it)? The cold chain sits underutilised. The logistics platform moves less volume than its unit economics require. The food processing facility operates at 40% capacity because the harvest it was designed to process is not arriving in sufficient quantities.

At that point, the investors who structured asset-backed debt against post-farm infrastructure face a question they did not model when the investment thesis was built. The assets are real. The infrastructure exists. But the returns depend on throughput. And throughput depends on harvests. And harvests depend on on-farm investment that nobody prioritised.

Could the post-farm investment thesis carry a hidden dependency on on-farm health that is not currently being priced into any model?

What is driving the assumption

Post-farm investors are not ignoring on-farm production entirely. The assumption appears to be that it will sustain itself (through smallholder farmer adaptability, through government agricultural programmes, through the indirect price incentives that better market access generates).

But could smallholder farmer adaptability alone be enough to fill a $117 billion capital gap? Could government agricultural programmes (in countries where those programmes are competing with debt servicing, security spending, and currency pressures for budget allocation) be relied upon to hold the upstream steady while private capital concentrates downstream?

And could the indirect price incentive mechanism work if farmers lack the mechanisation, inputs, and capital access to respond to better prices with increased production (even when that better route to market now exists)?

What if each of those assumptions is only partially right? What if the combined weight of all three partial failures is enough to widen the gap between what the downstream infrastructure was built to handle and what the upstream is actually producing?

What if the post-farm investment surge of 2024 and 2025 is building toward a correction (not because the infrastructure itself is flawed, but because the production base it was built to serve was never adequately capitalised in the first place)?

And if that correction arrives (if throughput falls short of projections across multiple post-farm platforms simultaneously) what does that moment look like for the continent's food distribution system?

The questions the next harvest cycle may begin to surface

The data today cannot yet confirm whether the pipeline paradox will materialise at scale. What it can confirm is that the structural conditions for it already exist. Capital is concentrated downstream. On-farm investment is declining. The financing gap is widening. And the hunger projections for 2026 suggest the production base is already under pressure from multiple directions at the same time.

2027 may be the year the infrastructure meets the harvest (and the gap between them becomes large enough to measure clearly in the data).

So the questions worth sitting with now are these.

What would it take for development finance institutions and policymakers to begin treating on-farm investment not as a development charity case but as the foundation on which post-farm returns actually depend?

What if a coordinated on-farm capital facility (designed specifically to address the $117 billion gap through blended finance instruments that do not require land titles as collateral) is not just a food security intervention but a direct protection mechanism for the post-farm investments already being deployed?

Who has both the analytical capacity to model this upstream-downstream dependency and the institutional mandate to act on it before the data confirms what it is already signaling?

And what does Africa risk if that question remains unanswered until 2027 makes it impossible to ignore?

This is the second in a four-part Prognosis Series examining the structural fault lines in African agtech investment. The next third release examines the Founder Burden (what happens to entrepreneurship in a sector where all the risk lands on founders and none on capital).