“I have $1 million. I’ll use $300,000 for residency by investment in Panama, $200,000 in Netflix, $100,000 in BYD, then hedge with another $100,000 in Tesla. I’ll buy a home in Atlanta for $200,000 and lock the rest in my Swiss bank account.”

Not one dollar of that money stays in Africa, even though it came from Africa.

For years, that script captured a common instinct among newly wealthy Africans. Once the first serious liquidity event arrived, the primary question was simple: “How do I move this to London, Dubai, or New York?” The moment a small boy becomes a big boy, his first defensive move is often to secure residency, assets, and savings overseas, not at home.

It is easy to frame this as a lack of patriotism. But the deeper question is structural: does the African policy and investment environment make it rational for that $1 million to stay?

From foreign discovery to domestic exposure

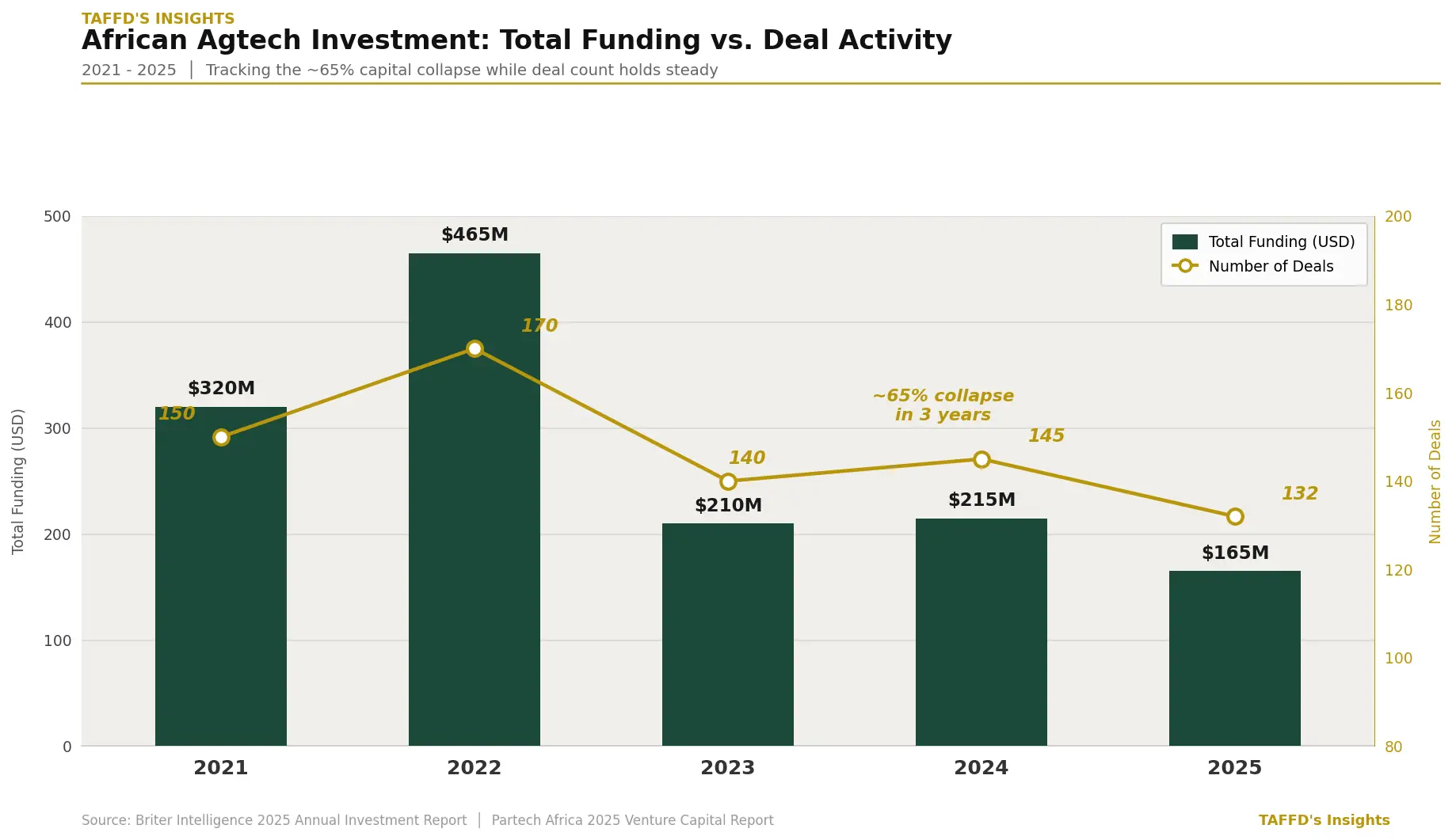

Between roughly 2016 and 2021, foreign capital “discovered” Africa at scale. FDI, development finance, and global venture funds pushed African startup and infrastructure funding to record levels, with disclosed startup funding surpassing $5 billion around 2021–2022. In those years, much of the risk capital validating African markets came from outside the continent.

Domestic capital, by contrast, largely remained on the sidelines. Many high‑net‑worth Africans continued to send their savings into foreign property, offshore accounts, and developed‑market equities. Africa was a place to generate returns, but not yet a place where local wealth chose to concentrate.

The global shock of 2022 exposed that imbalance. Inflation, rising interest rates, currency volatility, and the broader tech funding reset reduced the appetite of many global investors for risk assets in emerging markets. African startup funding volumes dropped from their 2021 peak, and some international funds paused new deployments or narrowed their geographical focus.

Inside the continent, this triggered a familiar fear: maybe “Africa Rising” had been more narrative than substance, dependent on fickle foreign interest.

A new funding mix

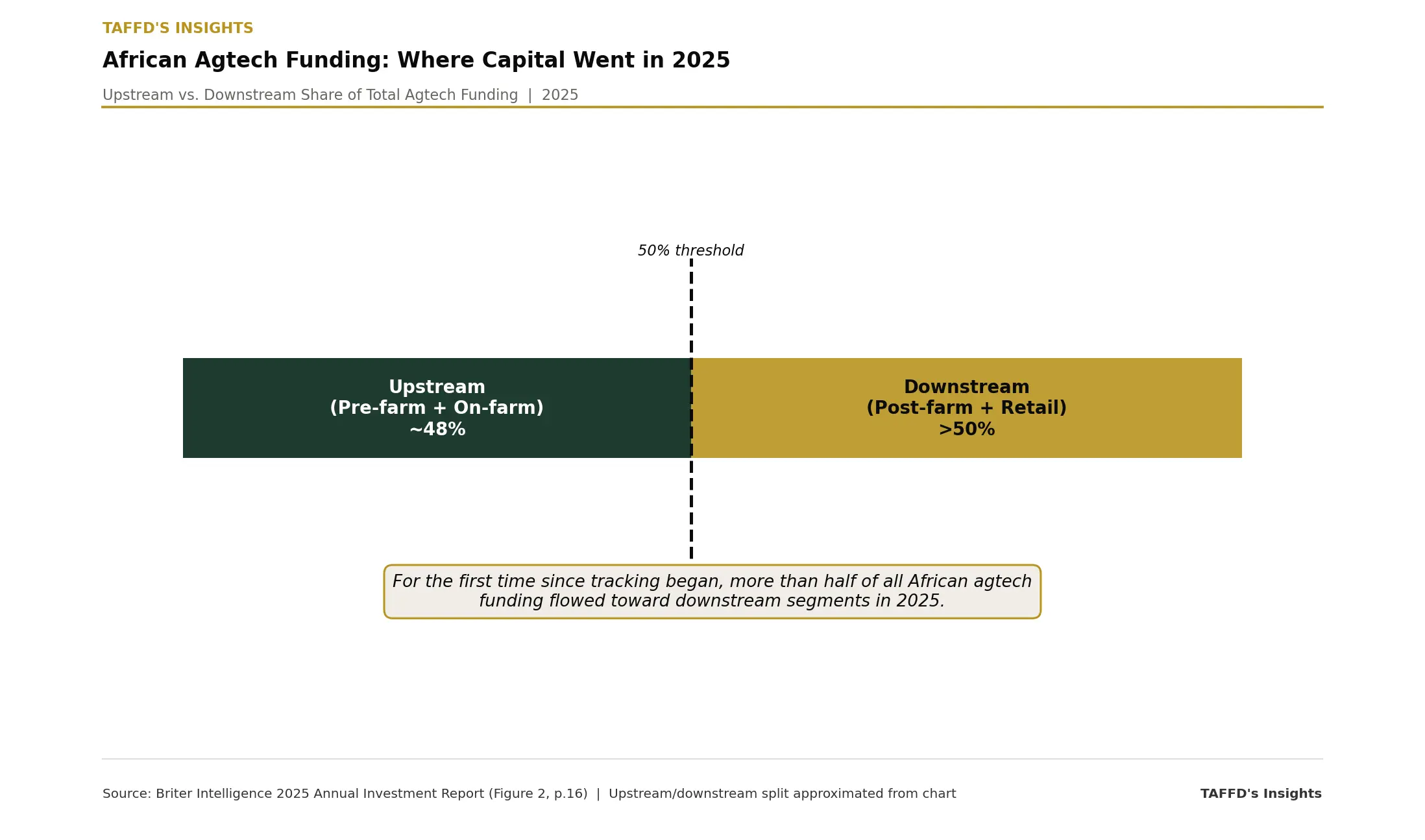

By 2025, however, the picture had begun to shift. According to Briter’s Africa Investment Report 2025, startups on the continent raised about $3.8 billion in disclosed funding that year, representing roughly 30–32% year‑on‑year growth after a cyclical trough. The distribution of that capital remains uneven. South Africa, Kenya, Egypt, and Nigeria still anchor most of the deal volume and value, while fintech and climate‑related infrastructure continue to attract the largest tickets.

The more important change lies behind the headline numbers. Recent analysis indicates that nearly 40% of African startup funding now comes from local investors, up from around 25% only a few years earlier. As foreign capital flows contracted from over $5 billion at their peak to roughly half that amount more recently, African capital stepped in. Domestic funds, corporate balance sheets, family offices, and angel syndicates have become central actors in keeping the pipeline of African companies funded.

In other words, the “who” behind the money is changing, even if the “where” still looks familiar.

From extraction to anchoring

This shift is significant because it signals a gradual psychological transition.

For much of the past decade, Africa functioned as a site of extraction. Local savings flowed out into foreign assets; foreign investors came in to chase growth and yield; exits and profits often left the continent again. Local investors often waited for foreign funds to validate markets before participating.

The recent rise in domestic participation suggests a different dynamic. African investors are increasingly willing to write early cheques, lead rounds, and absorb local risk. The $1 million that once defaulted to offshore structures is, in more cases, staying within African markets whether through funds, direct startup investments, or local infrastructure plays.

This is not yet a complete reversal. Many Africans still diversify abroad, and in macro terms, capital flight remains a persistent issue. But the direction of travel matters. For the first time, a meaningful share of venture and growth capital is being anchored by African decision‑makers who live with the consequences of local policy choices.

This has clear implications for regulators and regional institutions.

Policy systems built for foreign capital

African investment and financial policy frameworks were, for years, designed with external capital in mind. Incentives focused on attracting FDI, securing large anchor investors, and aligning with the mandates of multilateral lenders. Regulatory language and processes often assumed a foreign origin for serious capital.

The data now suggest that this assumption is out of date. If almost 40% of tech startup funding is now domestic, and if local investors are increasingly stepping in when global markets cycle down, the policy lens has to adjust.

Several gaps stand out:

- Capital formation: Many African markets still lack flexible vehicles for aggregating local savings into productive risk capital (for example, pension funds with venture mandates, local fund‑of‑funds structures, or tax‑efficient syndicate models).

- Risk sharing: Credit enhancement, first‑loss guarantees, and blended finance instruments are often calibrated for foreign institutions, not for domestic fund managers or angel networks that may have different constraints and fiduciary duties.

- Currency and exit policy: Macro‑prudential rules, listing regimes, and cross‑border investment restrictions can make it difficult to deploy local currency at scale or to recycle proceeds across African markets.

If policymakers continue to optimise primarily for foreign capital attraction, they risk overlooking the domestic investors who are now proving to be the system’s stabilisers.

Concentrated capital, concentrated risk

There is a second policy problem. Even as the origin of capital changes, its concentration patterns do not.

Briter’s data show that the same handful of markets and sectors receive the majority of investment. The “Big Four” ecosystems dominate funding. Fintech, digital payments, and capital‑intensive climate infrastructure capture repeated rounds. Meanwhile, smaller markets and non‑frontier sectors struggle to attract meaningful risk capital, even when they address critical national priorities.

If domestic investors simply replicate these concentration patterns, Africa trades one dependency for another. Foreign has become local, but exposure remains clustered.

The question then becomes: how can policy help shift from concentrated investment to distributed wealth?

Policy questions for the $1 million moment

As the $1 million mindset shifts from “leave Africa” to “build in Africa,” the policy agenda needs to reflect that change.

Three sets of questions are emerging:

1. How do we make distributed investment rational?

Early‑stage capital will not spread into smaller cities and new sectors purely on the basis of rhetoric. Regulators and DFIs can adjust risk‑sharing instruments, co‑investment schemes, and tax policy so that deploying capital in Kano, Kumasi, Kisumu, or Goma is not structurally penalised relative to Lagos, Nairobi, or Cape Town.

2. How do we de‑risk patient local capital?

If African pension funds, insurers, and sovereign funds are to allocate more to local venture and growth assets, they need clearer prudential guidelines, transparent data, and instruments that manage downside risk without eliminating upside. Blended finance and partial‑guarantee structures can be recalibrated to support domestic managers, not only international GP‑LP relationships.

3. How do we build information and narrative infrastructure?

Part of the “visibility and confidence” gap that pushed money offshore was informational. Granular data on performance, exits, and failures in African markets remains patchy. Platforms that track deals, map sector trajectories, and surface credible case studies backed by public‑private data partnerships, can reduce perceived risk for first‑time local investors.

These questions are not only for multilateral banks or ministries. Founders, investors, and ecosystem builders will shape the answers in how they structure funds, design products, and allocate attention.

If the money comes back, what then?

Over a month ago, I wrote about the $1 million African portfolio not to criticize those who diversify abroad, but to show how the narrative is evolving.

For a long time, the continent was treated primarily as a place to extract from, not to build in. Today, data from Briter and others suggest that local investors account for nearly 40% of African startup funding, and African capital is playing a larger role in keeping ecosystems alive through global cycles. That is a structural shift.

But if that money comes back and keeps landing in the same few places, policy has only done half its job.

The next phase is not only about retaining capital. It is about designing rules, instruments, and information systems that make it reasonable and attractive for that $1 million to be spread across more of the continent.

Only then can we say that Africa is not just the source of capital and the market for products, but also the place where wealth is built and held at scale.